Diminished Value | Turn Lemons into Lemonade : Diminished Value Car Claims A Quick How-To on Handling Diminished Value Claims

I. Introduction

It is well-known that most personal injury clients involved in a car wreck resulting in soft tissue injuries are more concerned with getting back on the road than their aching neck or sore back. Due to the lack of financial incentives for handling property damage claims, most personal injury attorneys shun away from representing clients for property damages altogether. With that in mind, a personal injury attorney can differentiate himself/herself by offering help on property damage claims and have the financial incentives as well through representing clients for their diminished value claims.

II. What is Diminished Value?

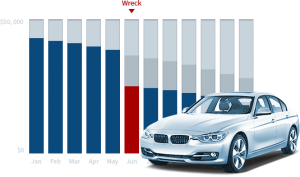

Diminished Value (“DV”) is the reduction in a vehicle’s market value after a vehicle is wrecked and repaired. In 2001, the Supreme Court of Georgia held that insurance companies are required to pay DV claims. (See State Farm Mutual Automobile Insurance Co. v. Mabry, 274 Ga. 498, 556 S.E.2d 114 (Ga. 2001)). DV claims are based on the reality that vehicles are worth far less after they are damaged in collisions—even after repairs are made. Most prospective buyers, whether they are dealerships or individuals, will not buy a wrecked and repaired vehicle. If they were to even consider purchasing it, they would demand a substantial discount. Like refurbished electronics, DV is a simple concept that EVERY judge and juror can understand.

III. How to Calculate DV

Insurance companies contend that the appropriate method for calculating DV is a formula called 17c. This formula comes from Mabry v. State Farm. The accurate way for calculating DV is simple. It is the fair market value prior to the accident minus the fair market value after the accident and repairs. For example, your car has a fair market value of $20,000 and unfortunately you are in a car accident on your way to work. After all proper repairs, the fair market value of your car has been reduced to $16,500. This means the diminished value of your vehicle would be $3,500. Why don’t insurance companies use this simple formula instead? The answer is simple; 17c favors the insurance company while hurting the victim of the accident.

Why the 17c Formula is Flawed

a. For starters, 17c allows for “double deductions” for mileage of a vehicle. Insurance companies use NADA to assess the fair market value of a vehicle. NADA already takes into account the amount of miles on the vehicle. However,17c includes an additional “mileage modifier.” This mileage modifier reduces the NADA value even more based on the number of miles on the vehicle. There is no reason to deduct more value for mileage when the NADA already considers mileage when making its estimates.

b. Another flaw in 17c is the use of a “damage modifier,” which takes into account the “nature and extent of the damages should be based on actual physical damage sustained by the vehicle, without using the cost to repair as a basis.” This statement makes absolutely no sense! It is impossible to accurately assess the damage of a vehicle without taking into account the cost of repairing the vehicle.

c. The damage modifier includes several options for the adjuster to evaluate the extent of damage, such as “severe, major, moderate, minor, and no structural damage.” This is a purely subjective form of assessment. Allowing the adjuster to choose from these ambiguous options is unfair to your client because the damage modifier does not consider the cost of repair to the vehicle. For these reasons, among others, 17c is NOT an accurate formula for calculating DV.

B. The Right Way to Calculate DV

There are no statutory guidelines for calculating DV. However, there is case law. According to Canal Ins. Co. v. Tullis, people seeking to recover for damage to their vehicle have two options to prove the amount of damage;

a. The difference of the fair market value pre and post collisions; and

b. The reasonable cost of repairs, with hire on the vehicle while rendered incapable of use and the value of any additional permanent impairment, provided that the aggregate of such amount does not exceed the fair market value before the collision

Calculating DV by these methods is simple and fair. It is a simple concept with simple math [(fair market value before accident) – (fair market value after repairs from accident) = DV]. It is only fair that your clients receive the decrease in value to their vehicles as a result of the collision.

IV. Best Way to Prove DV

According to O.C.G.A. § 24-9-6, one need not be a dealer or an expert to assess the value of the vehicle. However, the best way to determine the DV of a vehicle is to hire a reputable independent appraiser to assess the DV of the vehicle, such as Tony Rached of Diminished Value of Georgia .

V. State Farm Insurance’s View on DV

State Farm continually sends our clients DV checks coupled with the Mabry v. State Farm letter saying a DV assessment has been made “using a formula authorized by the Mabry trial court.” Invariably, these initial DV checks are a mere fraction of the actual DV amounts. State Farm is wrong in this regard (see Mabry v. State Farm and Office of Insurance and Safety Fire Commissioner Directive 08-P&C-2). Our purpose is to stop State Farm from ignoring and abusing the law!

VI. First Party and Third Party DV Claims

First party DV claims result when an insured files a claim with his/her insurer under the collision coverage. First party claims are governed by contract law and are based on the contractual relationship between the insured and the insurance company. On the other hand, third party diminished value claims result when a third party files a claim against the at-fault party’s insurance company. Third party diminished value claims are governed by tort law because there is no contractual relationship between your client and the at-fault party’s insurance company.

VII. Tips on DV Claims

Based on our experience, DV is positively correlated to the amount of repair and negatively correlated with the age of the vehicle. The more repair a vehicle needs the more DV it has and the older the vehicle is the less DV it has. Choose your DV cases carefully. In our opinion, DV exists for most types and ages of vehicles but it is not cost effective to demand for DV on vehicles more than 10 years old or with less than $ 1,500.00 in repairs. With help from senior GTLA members, Gary Martin Hays and Richard S. Alembik, we were shown the way! Here are some tips on how to handle DV claims:

A. Tips on First Party DV Claims under O.C.G.A. § 33-4-6

1. Obtain an independent DV appraisal from a reputable appraiser immediately after the wrecked vehicle is repaired using the final repair bill.

2. Gary Martin Hays suggests that you also have your client take the final repair bill and vehicle to CarMax and ask them to appraise the vehicle (read his article “Diminished Value Claims: Tell the Insurance Companies Where They Can Stick Their 17c Formula”—Genius!). Proof of DV can also be done through the owner–someone who had an opportunity to form a correct opinion.

3. Once you have the DV appraisal, send a demand that complies with O.C.G.A. §33-4-6 to your client’s insurance carrier.

a. Under this statute, the insurance company has 60 days to review this demand before you can file suit.

b. Within this 60-day period, the insurance company is allowed to inspect your client’s vehicle and may make offers to settle the claim.

4. If the insurance company refuses to offer your client a reasonable settlement at the expiration of the 60-day time limit period, file suit in State or Superior Court (the more attorneys that are holding these insurers accountable, the better it will be for all of us).

5. In the first party claim, you do not have to hit your demand amount in order to recover bad faith. If the jury finds bad faith, you will recover 50% of the DV amount or $ 5,000.00 (whichever is greater) as a penalty and reasonable attorney’s fees. Instead of paying the DV amount demanded earlier, the insurer is now exposed to much greater liability (an amount that can be as much as $ 25,000.00).

· amount of DV;

· maximum {$ 5,000.00, 50% of DV claim}; and

· reasonable attorneys’ fees for the prosecution of the claim.

6. Offer of Judgment cannot be utilized in a first party claim because it’s a breach of contract claim under O.C.G.A. § 33-4-6 (O.C.G.A. § 9-11-68 only applies to tort claims).

7. You may not seek attorneys’ fees under O.C.G.A. § 13-6-11 for a first-party DV claim either.

B. Tips on Third Party DV Claims under O.C.G.A. § 33-4-7

1. Obtain an independent DV appraisal from a reputable appraiser immediately after the wrecked vehicle is repaired using the final repair bill.

2. Send a demand letter pursuant to O.C.G.A. § 33-4-7 with a 60-day time limit.

a. Make sure you demand an amount that you can prove.

b. We suggest discounting the appraisal amount by 10% or so. For example, if the DV appraisal is $ 3,000.00, you may want to demand $ 2,700.00. If the jury comes back with an award of $ 2,800.00, you can still proceed with the bad faith claim.

3. If there are no reasonable offers to settle within the 60-day time limit, file suit in State or Superior Court.

4. Name the insurer as an unnamed defendant pursuant to O.C.G.A. § 33-4-7(a).

5. Pound them with ROGS, RFA, and RFP to both the at-fault driver and his/her insurer!

6. Under O.C.G.A. § 33-4-7(d), once you secure a verdict equal to or in excess of the DV amount demanded then the trial is recommended to the jury to hear evidence of bad faith.

a. Reasonable attorney’s fees can be recovered.

b. A penalty of 50% of the DV amount or $ 5,000.00 (whichever is greater) can also be recovered.

7. Punitive damages may be sought for egregious conduct such as DUI.

- Article written By Hung Nguyen & Rebecca K. Sapp, Atlanta Personal Injury attorneys.

To learn more about Diminished Value, please call us at 678-805-4066 or fill out the form below. Thank you.